| The Monetary Policy Committee voted 7–2 to leave Bank Rate unchanged at 3.75% at its June meeting | Official figures suggest consumers returned to the high street during May, with warmer weather helping lift retail activity | UK Consumer Price Index inflation held steady at 2.8% in May, defying analyst forecasts of 3.0% rise |

Bank of England keeps rates steady as stronger Q1 growth revealed

The Bank of England’s Monetary Policy Committee (MPC) voted 7–2 to leave Bank Rate unchanged at 3.75% at its June meeting, a decision widely anticipated by a Reuters poll of economists.

The outcome came against a backdrop of heightened political uncertainty at home and overseas. Mid-month, Keir Starmer announced he was resigning as Prime Minister and Labour Party Leader, potentially leaving the way clear for Andy Burnham to become the new PM, if uncontested. It also came shortly after a tentative ceasefire agreement between the US and Iran.

Following the MPC meeting, Bank of England (BoE) Governor Andrew Bailey warned that recent energy price increases were likely to continue feeding through into inflation, despite the fall in oil prices. He noted that, “Oil prices have fallen in recent days, and that’s encouraging, but they’re still higher than before the war.” He continued, “Whatever happens in the future, the higher energy prices of the past four months mean there’s already some inflationary pressure in the pipeline.”

Against this backdrop, June’s updated figures from the Office for National Statistics (ONS) gave some reassurance on near-term activity, albeit with a mixed underlying picture. The UK economy grew by 0.6% in Q1 2026, with output 0.9% higher than a year earlier. Revisions to historical data also indicate that growth in 2025 was slightly weaker than first thought, at around 1.3% overall. Commenting on the figures, ONS Director of Economic Statistics Liz McKeown said growth “picked up in the first quarter… led by broad-based increases across the services sector,” highlighting a relatively strong start to the year.

Attention will soon turn to the MPC’s next meeting on 30 July as an indicator of whether this improvement in growth can be sustained.

Retail sales rebound as warm weather boosts spending

Official figures suggest consumers returned to the high street during May, with warmer weather helping to lift retail activity after a weaker April.

According to the latest ONS data, retail sales volumes rose by an estimated 0.4% over the three months to May, while monthly sales increased by a stronger-than-expected 1.2% (estimate). The recovery followed a revised 1.0% decline in April and a revised 0.7% increase in March.

Retailers attributed the rebound to promotional activity and the hot weather, which helped boost sales at department stores and online retailers. For example, food and grocery stores reported higher sales of barbecue and picnic-related items, while clothing retailers benefitted from increased demand for lighter seasonal ranges. However, the weather-related improvement has left some experts warning that consumer discretionary spending remains subdued.

According to GfK’s Consumer Confidence Index, June’s recording was unchanged at -23%, although confidence among the 16 to 29 age group dropped 11 points from the previous month. Looking ahead, views on personal finances are flat, while the backwards-looking measures on personal finances and the economy are both down, reflecting the challenges faced by many over the last year.

Commenting on the data, Harvir Dhillon, Economist at the British Retail Consortium, said that despite the short-term boost provided by the weather, “retailers continue to face significant challenges.”

Given stretched household budgets, fragile consumer confidence and increasing operating costs, he added, “To support growth and help keep inflation under control, government must address the taxes and levies that are increasing energy costs for businesses. Without intervention, mounting cost pressures will make it harder for retailers to invest, grow and keep prices affordable for customers.”

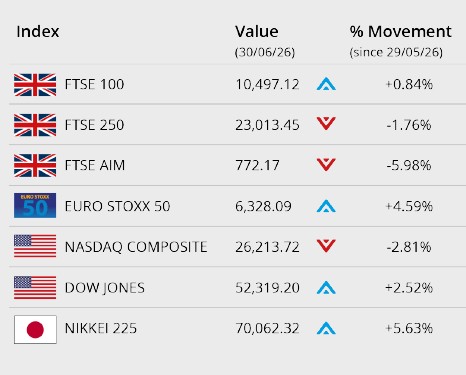

Markets

As Q2 drew to a close, major global equity markets ended June in mixed territory. US stocks rose as investors weighed a strong performance in chip stocks in the first half of the year and the dollar’s growing strength, while attention turned to the upcoming earnings season.

Wall Street rallied as easing tensions between the US and Iran improved investor sentiment. The Dow Jones gained 2.52% in June to close on 52,319.20, posting a fresh record after the blue-chip benchmark closed above 52,000. The tech-focused NASDAQ recorded a monthly loss of 2.81% to close on 26,213.72 but registered a solid quarterly gain on the back of the chip stock rally.

In the UK, at month end, outgoing Prime Minister Keir Starmer unveiled an extensive £15bn Defence Investment Plan which provided support to the sector. The FTSE 100 closed June up 0.84% on 10,497.12. Meanwhile, the FTSE 250 ended the month 1.76% lower on 23,013.45 and the FTSE AIM recorded a loss of 5.98% at month end to close on 772.17. The Euro Stoxx 50 closed June 4.59% higher on 6,328.09. In Japan, the Nikkei 225 closed the month on 70,062.32, gaining 5.63%.

On the foreign exchanges, the euro closed the month at €1.16 against sterling. The US dollar closed at $1.32 against sterling and at $1.14 against the euro.

Brent Crude closed June at around $73 per barrel, recording a monthly loss of nearly 20%. Oil prices fell in the month as the Strait of Hormuz reopened, easing concerns over oil supply disruptions. The US and Iran signed a memorandum of understanding to pause the conflict and negotiate a broader agreement, although implementation remains fragile. Gold closed the month trading around $4,044 a troy ounce, a loss of over 11% in June, as persistent inflation concerns and prospects of further interest rate increases reduced demand.

UK inflation dips unexpectedly below forecasts

ONS announced that UK Consumer Price Index (CPI) inflation held steady at 2.8% in May, defying analyst forecasts of a 3.0% rise.

The unchanged rate was attributed to a slower rate of food price rises, particularly meat, dairy and vegetables, which unexpectedly reached a new 17-month low. However, transport costs made the largest contribution to higher prices, rising by 6.8% in May from 4.5% in April, as airfares and motor fuel prices rose. These rises were attributed to the energy shock from war in the Middle East, plus increased demand over the busy school holiday period. Core CPI inflation, which strips out energy, food, alcohol and tobacco from the data, rose by 2.6% in the 12 months to May, up from April’s 2.5%.

After June’s MPC meeting, the BoE Governor predicted a “slow return” of inflation towards its 2.0% target and suggested inflation could reach 3.3% before the end of the year. James Smith, Chief Economist at the Resolution Foundation, said, “Signs of peace in the Middle East mean that energy prices have tumbled. This likely reduces pressures on struggling families this winter and reduces the likelihood of rate rises from the Bank of England.”

PMI data points to softer business activity

The UK’s business output weakened in June, according to the mid-month flash purchasing managers’ index (PMI) reading published by S&P.

S&P’s Composite PMI, which measures the overall health of the UK’s private sector, ticked down from 49.7 in May to 49.4, the lowest level in 14 months (a reading below 50 represents a contraction). Business activity in the services sector slumped to a 41-month low of 48.7, down from 49.3 in May. The fall in demand was driven by weaker consumer discretionary spending and delayed spending from businesses, as war in the Middle East, the resulting energy shock, plus political uncertainty at home dampened sentiment. Output in the manufacturing sector was brighter, rising from 52.2 in May to 53.6 in June, a 21-month high, although this was attributed to companies stockpiling ahead of potential price rises for goods.

Commenting on the data, Chris Williamson of S&P Global Market Intelligence, said, “For the growth and inflation outlooks, much depends on progress towards an end to the conflict in the Middle East, but closer to home we are seeing signs of the unstable political environment unsettling business confidence and delaying spending, which will also need to calm in order to lay better foundations for economic growth to revive.”

All details are correct at the time of writing (01 July 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.